Foreword by the Vice President (Research & Enterprise), Professor S. Mark Spearing

Following an extensive consultation with academic staff, spinout founders, the University’s Entrepreneurs-in-Residence, investors and other key stakeholders in spinout success, the University of Southampton is launching an updated Spinout Equity Guide.

Driven by our vision and strategic objectives for enterprise, the University shall take equity in new spinout companies at an investor attractive and key founder friendly level with a principal aim of boosting this important economic impact generating activity. However, it is also essential that we ensure all support to our spinout formation activities remains at a financially self-sustainable level, hence reviews shall be conducted (at 3-year intervals) in the future to evaluate the achieved and future intellectual property fees and return from equity as a consequence of this change.

I thoroughly support this new Spinout Equity Guide and wish to see many more spinouts emerge from the fantastic research and innovation work going on in our Faculties. Our new equity levels are extremely progressive and ambitious and compliant with the Independent Spinout Review recommendations, and I hope it encourages our innovators to consider the spinout route.

What is the new Spinout Equity Guide?

The new Spinout Equity Guide outlines the level of equity that the University will take in new spinout companies (See Table 1).

When a university spinout company is created the sharing of equity is agreed between the founder researchers and the University. New arrangements for institutional and individual founders equity sharing are now being implemented.

This Guide aims to improve the experience of spinout founders, incentivise academics and researchers to take part in spinout activity, provide improved terms for spinout founders to maximise their company’s chances of success and enhance the speed of deal making by removing previous barriers to concluding negotiations.

This Guide aligns with the TenU USIT Guides and is fully compliant with the recommendations of the Independent Spinout Review.

Table 1: New Guide University Spinout Equity Levels

Spinout category

University of Southampton initial equity allocation

Knowledge intensive spinouts

10% equity

Software spinouts

5% equity

Knowledge intensive spinout

Knowledge intensive spinout means where there is significant University intellectual property (IP) involved. This may include, but is not limited to, patents or patentable inventions, significant confidential know-how, and or significant other non-patent IP, other than Software. It may also include, where the University has provided significant initial institutional support to the generation of relevant IP. For example, significant infrastructure, salary support, IP protection expenses and innovation or translational funding. This may take the form of Higher Education Innovation Funding (HEIF), UK Research and Innovation (UKRI) Impact Acceleration or seed investment funding. It may also include, where there has been material research funding from a third party for the relevant University IP.

Software spinout

Software spinout means where there is Software IP involved (where other minor know-how directly supporting the Software may also be included) and there has been very low initial institutional funding or other infrastructure support (such as high performance computer resource) provided in the generation of relevant IP and where there is nil or negligible research funding from any third party funder.

Further details on how the University will decide on this classification is described further in Section 4 below.

The decision to reduce institutional founding equity from 33.3% to either 10% or 5%, was made to be founder-friendly and to increase investor attractiveness for the University’s early-stage new spinouts.

Note, the figures quoted in Table 1 are applied where the University of Southampton is the exclusive owner of IP to be licensed to the spinout and there is no collaborating partner institution involved, including any inventors from a collaborator.

If the background research and IP generation was collaborative with other institutions, then the University will work with its founders and other institution(s) to agree a founding equity allocation that may vary from the Table 1 figures above. This is further detailed in Section 6.

The remainder of this page explains why the Spinout Equity Guide is being introduced, what it means for new University spinouts and for those having already started the process of being created.

The new Guide sets the founding equity share in spinout companies at 90% for founder researchers and 10% for the University. These equity percentages are applied when the spinout is classed as a knowledge intensive spinout company. When the spinout company is classified as a software spinout, the founding equity share will be 95% for founder researchers and 5% for the University.

In certain circumstances involving third parties or other cases, some additional calculation factors will be involved, this is explained further in points 5, 6 and 12.

This guide’s new equity levels reflect the University’s commitment as a ‘triple helix’ institution to further strengthen our enterprise and knowledge exchange activities. We aim to grow our business and economic impact through supporting innovation and our entrepreneurial founders to maximise the global impact of the University’s research and expertise. We hope this progressive stance will be an attractor for new staff, students and potential investors.

The guide is an open, transparent statement to researchers and investors about equity sharing arrangements. It emphasises an equity stake for the University at the lower end of the USIT Spinout Guide recommended range, which enables the spinout to incentivise founder researchers and attract experienced management teams and investors. It removes the need for prolonged negotiations in all cases which will make spinout formation faster, easier and more transparent.

The Guide will be in operation as from 31 May 2024. The University expects to apply the new Guide to all spinout companies progressing towards completion, presuming that the relevant founders are content with this proposal.

The University recognises that different spinout company types have differing levels of historic institutional support in the research that created the relevant IP. Also, the IP types themselves reflect different levels of commercial value with patents being regarded highest amongst industry and investor organisations.

Spinout companies have varying investment funding profiles and development timeframes to reach their respective markets. They may generate greater commercial and technical progress through high quality talent hiring and have less reliance on core licensed University IP that is developed post spinning out. These factors have been covered in detail in the USIT Spinout Guide and USIT Guide for Software.

Due to these different profiles, some companies are better suited to differing, appropriate arrangements of equity rewarding and overall shareholder allocations. The University of Southampton has considered all these factors during its consultation activity and supports the conclusion of the USIT Guides. The University’s new guide has 10% University equity allocation for knowledge intensive spinout companies (in the first USIT Guide recommended range) and a 5% University equity allocation for software spinouts (in the USIT Guide for Software recommended range).

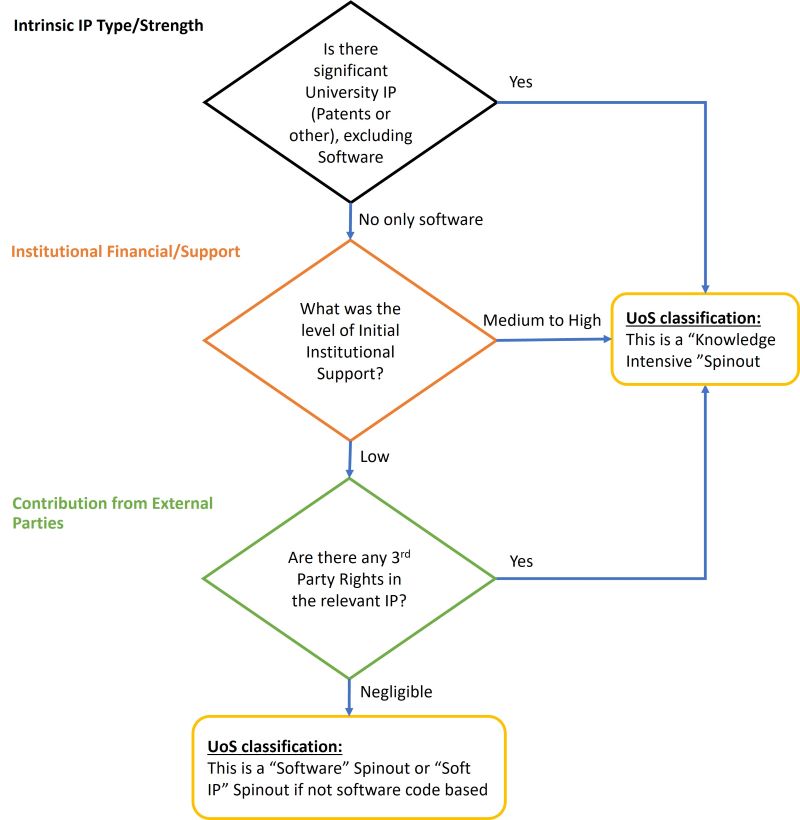

At Schedule 1- Part A, we include a decision flow diagram to be used for categorising a new spinout as either a knowledge intensive spinout or as a software spinout.

Research and Innovation Services department of the University will work with founder teams and involving any supporting investors at that time and shall advise how the decision flow diagram has been applied in each specific case. The decision shall be made and confirmed prior to seeking the approval in principle for spinout from the University’s Knowledge Exchange and Enterprise Board (KEE Board). In the event of any founders’ disagreement on classification at this stage, the matter may be escalated within the University up to the University’s Knowledge Exchange and Enterprise Board and any final decision shall be made by the Vice President, Research and Enterprise.

The University has deliberately set the equity levels at the lower end of recommended ranges to progressively encourage quick negotiations and reach agreement on spinout commercial terms.

If the spinout founders decide to include external individuals who are not University employees as members of the founding team (for example as a CEO or other key post in the Company), those individuals will share in the 90% or 95% that the researcher founders are expected to allocate at formation. This includes the issue of shares or the creation of option pools for management teams at formation prior to any funding round. The University will be diluted along with all other shareholders by any subsequent option pool that is put in place after a funding round for employee incentives.

Where the University is required to share any part of its institutional founding equity with a third-party research funder, this reduction of the founding equity held by the University will normally be borne pro-rata by the University and the founders.

In some cases, relevant IP to be licensed may involve historic collaborating institutions and their inventors. Where these institutions and external inventors are not involved in the Company, then, the University shall agree a fair and reasonable revenue share with the collaborating institution in consideration of the University being given the exclusive right to commercialise IP through the Spinout Company. The revenue share allocation to the other institution(s) shall be borne pro-rata by the University and the founders.

In Schedule 2, Table 3 and 4 show how the pro rata calculations work. These show post revenue share allocations to founders, the University and revenue sharing organisation, for the case of a Knowledge Intensive spinout (90% to 10%) and a Software spinout (95% to 5%), respectively.

In almost all revenue share cases, such third parties will not directly hold shares in the Company themselves, but these are held on account by the University (on behalf of the third party). Therefore, such third party would be expected to enter into a revenue share agreement with the University and at the time of any payment received by the University from or resulting from the Company, then, the University would pay the relevant proportion of that money on to the (revenue sharing) third party.

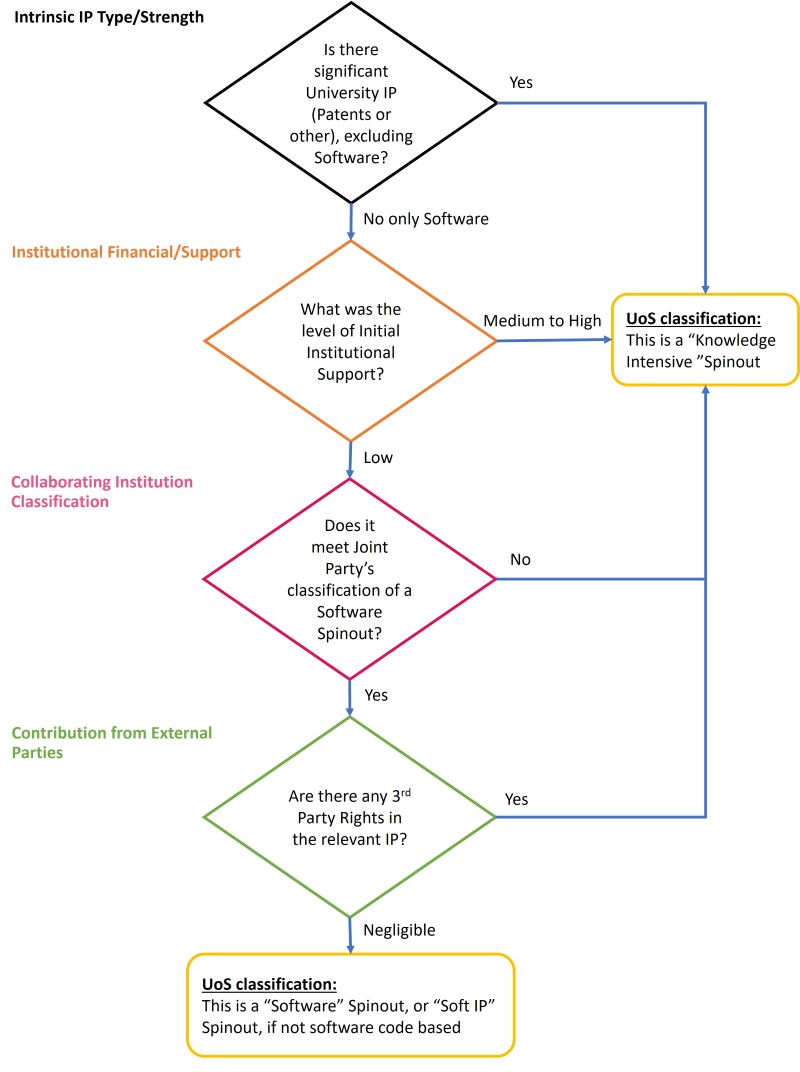

Where other institutions and their inventors are playing a significant role in the spinout, including generating the relevant IP, then these would be regarded as additional founding-institution shareholders. In which case, the standard equity levels will need to be modified to take account of the other institution’s spinout equity approach. The University will work with its founders and other institution(s) to agree a founding equity allocation that fairly reflects all the relative contributions to IP generation and all company founding roles. This mutual agreement may require variation from the Table 1 figures.

The Decision Flow Chart 2 (in Schedule 1 – Part B) will apply to Spinout Classification in such cases with other founding institutions.

Both company founders and any such researchers or technical staff are covered by the University’s Intellectual Property regulations , hence all these individuals will be rewarded for the spinout’s future use of the IP (through the IP Licence Agreement).

The University acknowledges that equity reward is primarily focused on creating future value in the spinout. Founders should recommend to the University the allocation of:

a) shares that are a reward for contribution to creation of the IP and or know-how

b) shares used to incentivise taking the Company forward by those founders involved

In the case that a) allocates equity for non-founders, this shall form part of the share (either 90% or 95%) that the researcher founders are to allocate at formation.

In recognition of the substantial allocation of initial equity to themselves, company founders and other University member shareholders will waive their rights to receive any other share from University royalties or from proceeds of share sales (from that spinout) that it may receive in the future.

If the IP licence agreement between the University and the Spinout is field limited, and the University licences (out of field) the IP to another organisation, then standard inventor distributions apply for such additional licence fees.

The following further Intellectual Property Fees will also be included in any spinout IP Licence and are aligned with the ranges published in the USIT Guides. These fees have been decided with the key aim to assist in early-stage company financial sustainability, while sharing a fair and reasonable proportion of the return from its later stage commercial success.

IP Royalty and Other Fees:

Licence Fee: This is a flat fee of £100k payable in five annual instalments following the third anniversary of licence date (£20k each year).

Royalty Fee: A percentage royalty on net sales commencing from the third anniversary of the licence date. The Royalty fee will be dependent on the Technology Readiness Level (TRL) of the IP as well as the type of spin out (ie Knowledge intensive or Software), see Table 2.

Table 2: Guide to royalty fees

For early stage technologies with low TRL for knowledge intensive spinouts and for all software spinouts

1% to 2%

For medium TRL

2% to 5%

For higher TRL and as appropriate for relevant technology type and industry

5%+

Note: For early stage technologies, the USIT Guide is 0% to 2%, however, this has been re-stated here as 1% to 2% due to the University of Southampton’s equity position which is at the bottom end of USIT recommended range.

Sub-licensing: A 10% revenue share of net receipts from any licensee sub-licensing income received.

Milestone and Success Fees may be appropriate on a case by case basis depending on the nature of the IP and, also taking account of situations where the University may have taken greater equity (see section 12), and the number of licensed patents. Hence, these fees will be negotiated where appropriate.

Patent Expenses: Where a spinout company takes a licence to a patent or patent application then, the existing practices will continue to apply;

The Company shall be liable to reimburse all patent expenses from the date of the licence and

The Company and University shall agree a repayment schedule for reimbursement of historical patent expenses, this is expected to be triggered by a significant later investment round.

We are wanting to ensure the spinout gets equitable and appropriate access to other IP that may provide the spinout with greater chances of future success but also to ensure fair return to other inventors/creators of the new IP and any terms agreed to fairly reflect all relevant support for new IP generation. We also want to ensure that other IP has the best chance to be progressed and is only licensed where there is a commitment to take it forward.

Therefore, licence rights to non-severable improvements of the licensed technology (the ‘technology pipeline’) will be incorporated into the IP licence agreement but this will be time limited. These would be focused on unencumbered founder generated IP and not more widely generated across the University. Other University IP generated by the founders or their research group may be offered at a future stage where the University believes it is relevant to the spinout and the Company has the capacity to take forward. The terms for this would be negotiated at the appropriate time and a separate licence entered into.

The University’s primary objective from IP commercialisation activities, such as creating spinouts, is to help create business and economic impact. The level of financial return remains important to the extent that as a charitable organisation we must balance sources and uses of all income. This includes making an assessment on the balance of institutional reward and risk-adjusted individual incentives provided to key personnel. As a public body, the University’s return overall must be fair, reasonable and non-discriminatory to ensure fair competition is ensured for the use of University owned intellectual property.

The University recommends that equity compensation is an appropriate mechanism for early stage start-ups as it reduces the amount of (licence) fees being paid out during critical company technology and market development stages.

Further, many University spinouts initially remain located in their founding research departments and key personnel often wear ‘dual hats’ for example, through University consultancy, secondment or collaboration services, therefore, a meaningful equity allocation is highly aligned with the strategic partner and governance relationship with the founding institution.

The University has set these equity levels with the intention to reduce lengthy negotiations on equity. They are at the lowest end of the respective USIT guides and extremely founder friendly and therefore the University is not open to reducing to a lower level.

Where founders and or investors want to remove or further reduce IP licence fees and or get increased rights to future IP, then, we can enter into discussions to increase the equity level to accommodate such objectives.

The University is adopting this guide for the next three years, after which there will be a review (see Section 17). The University may decide to change the Guide if we are not seeing the level of income we need to sustain all our Spinout focused activity. The University is not looking to negotiate greater equity levels save in exceptional circumstances.

Two examples of when we might exercise an exception are:

a) Where we licence a significant bundle of intellectual property and knowledge assets (multiple patents). We may seek slightly higher equity but we will adhere to USIT guide landing zones.

b) Where we have an existing enterprise or commercialisation activity which has been significantly incubated within the University such that we already have customers and revenues and we employ staff specifically to service this activity. In this type of case, there are numerous factors to consider in addition to IP (including TUPE) and of course goodwill and existing value that has been created. Therefore, whilst some of the principles in this Guide will be useful, we reserve the right to assess the benefits and structure for spinning out this type of activity separately from this Guide.

Additionally, in some cases the University may decide to hold no equity in a spinout company. This is typical where, despite being a viable ongoing business activity, the University’s assessment is that there is no or minimal prospect of achieving a financial return from holding equity. In such cases, the University shall licence the relevant intellectual property on fair and reasonable arms-length terms. This practice has been in place at the University previously and shall continue under the new Spinout Equity Guide.

The University wishes to increase the speed of completing spinout deals and supports the recommendations from the USIT Guides and the Independent Spinout Review. It is actively working on refreshing a number of spinout legal agreements. Working efficiently with all other stakeholders and their advisers is critical in seeking to create spinout success.

If all parties are appropriately prepared and engage constructively, then the University would seek to reach agreement with all other parties on spinout heads of terms in no greater than two months. Following that, a further two months will be needed to conclude all final legal negotiations and execute completion proceedings.

Different spinout cases may have varying levels of complexity including, for example, a new spinout sponsored collaboration agreement with the University, the spinout taking laboratory and or office space in a host department, or one of the academic staff taking a partial secondment with the spinout. Dependent on the complexity and scope of all agreements required for a specific spinout, the timelines may approach the timelines above in more complex cases, but in many cases would be able to take place more quickly due to the new Spinout Equity Guide.

Our current practice is that all equity holdings are held by the University directly. The University reviews the group structure approach regularly and may consider structuring holdings in spinouts to be in a wholly owned subsidiary. We will also reserve the right to move holdings from the University to such an entity in any legal documentation we enter into for the formation of the Spinout Company.

In the event that a spinout company shares are sold or produce income such as dividends, then, after sharing with relevant third parties (as described in section 6) above, these returns are used for initiatives, projects and services across the entire University, for which many do not have a guaranteed financial return, such as supporting Faculties, departments and investing in strategic research and innovation initiatives and projects.

These major investments will be developed by the relevant department or Faculty and approved by Knowledge Exchange and Enterprise Board and Finance Committee, where appropriate.

A key principle for all IP commercialisation net returns received by and retained after appropriate distribution by the University is that 50% is shared with the relevant founding Faculty and 50% retained by central University for the purposes described above.

Anti-dilution provisions will not apply to these University founding shares. The University will take ordinary shares and will be diluted along with other founder shareholders as investment comes into the Company. Having taken appropriate consultation, the University believes non-dilutable shares are unhelpful in attracting future investors.

Yes, the University will evaluate the success of implementing the new Spinout Equity Guide. Its assessment shall include the number of companies being formed, the investment levels being achieved, company valuation levels and the success of negotiating equitable licensing royalty fees. The intention of this strategic change is to drive long-term spinout performance and hence the evaluation shall be conducted every three years going forwards.

To ensure that the University continues to receive appropriate returns, in order to invest further in research and innovation, it is expected that companies will raise investment at valuations which are at least comparable to those achieved before this Guide change.

Some investor feedback raised during the consultation exercise was that larger holdings for non-participating shareholders may drive valuation readjustments in later investment rounds. However recent data, from the Policy Evidence Unit for University Commercialisation and Innovation, Cambridge , indicates that founding equity level has little or only very modest effect on subsequent investments.

It is hoped that the new University equity level will stimulate more spinouts that are attractive and competitive and set them up for successful future investment rounds.

While the University believes this will result in greater future success, the medium to long-term investment profile of spinouts and valuation levels, including incidence of ‘downround’ valuations will be evaluated in the triennial reviews.

Schedule 1

Decision making flow diagram for 'knowledge intensive’ or ‘software’ spinout classification.

University of Southampton and its founders, only, involved in prospective Company (Decision flow chart 1)

University of Southampton, its founders and collaborating institution and its own founding shareholder involved in prospective Company (Decision Flow Chart 2 – University of Southampton leading)

Schedule 2

Standard tables showing pro rata factors for revenue sharing party obligations

Knowledge intensive

Table 3: Pro rata calculation table for Knowledge Intensive spinouts (Founders, University and Revenue sharing third party)

Revenue share (%) level

10%

15%

20%

25%

30%

40%

50%

10% equity

Founders

89.1%

88.65%

88.2%

87.75%

87.3%

86.4%

85.5%

University

9.9%

9.85%

9.8%

9.75%

9.7%

9.6%

9.5%

Third party

1%

1.5%

2%

2.5%

3%

4%

5%

Royalty per revenue share

University

90%

85%

80%

75%

70%

60%

50%

Third party

10%

15%

20%

25%

30%

40%

50%

Software spinout

Table 4: Pro rata calculation table for Software spinouts (Founders, University and Revenue sharing third party)